One of the basic tenets of valuation is the value of any asset is a function of the future cashflows from that asset. This principle applies to income based valuations like Future Maintainable Earnings, where an income stream is expected to continue indefinitely into the future or market based valuations (Net Realisable Assets) where the expected value is what can be realised now.

The Future Maintainable Earnings methodology is in fact a simplified version of the Discounted Cash Flow Methodology in which a number of assumptions or variables are removed.

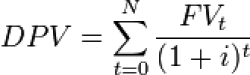

The Discounted Cash Flow methodology assumes that the value of a business (or asset) is the sum of the present value of its expected future cashflows discounted for return and risk.

The DCF analysis requires assumptions or projections to be made about future income and expenditure (including capital expenditure) in achieving or maintaining that income and the application of an appropriate discount rate to calculate the present value of those future cash flows.

The forecast period in a business valuation normally is of such a length to enable the entity to achieve a stabilized level of earnings, or to be reflective of an entire operation cycle for a cyclical industry. In mining valuations, the projection may be to the end of the useful life of the mine. In businesses that are expected to continue or have no definite end, the forecast period is generally 10 years, but in those instances it is necessary to include a terminal value. The terminal value is calculated on the basis that the business is sold at that point. In effect it does require another valuation - a valuation within a valuation.

In calculating the cash flows of a business, it is necessary to distinguish:

The are a number of difficulties in applying the DCF approach in small business valuations - the primary on being that there is rarely sufficient financial information available that would enable a DCF valuation to be worthwhile without making the same assumptions inherent in the Future Maintainable Earnings methodology.

{kind=link}