.png?width=1024&height=768&name=Blog%20Post%20Templates%20(21).png)

Big Changes Coming with the 2025 Banking Code of Practice

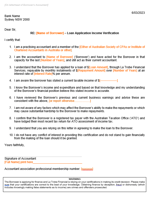

Australian accountants will soon no longer be asked to certify their small business clients' ability to repay loans, thanks to a key update in the 2025 Banking Code of Practice issued by the Australian Banking Association (ABA).

Effective 28 February 2025, ABA member banks will stop requiring capacity to repay certificates, also known as accountant’s declarations, shifting full responsibility for loan assessments back onto lenders.

Clause 78 of the revised Code explicitly states:

“We will not ask a third party (such as your accountant) to certify that you can repay the Loan.”

This is a major win for accountants, who have long been placed in difficult positions by lenders and clients requesting these declarations. However, risks remain, particularly for practitioners dealing with non-ABA lenders who may still request these letters.

Why This Change Matters for Accountants

For years, the capacity to repay certificates has been a contentious issue in the accounting profession.

- Increased pressure from lenders – In recent years, as economic conditions have tightened, many small businesses have struggled financially. In response, lenders increased their reliance on accountants’ certifications, leading to greater pressure on practitioners.

- Legal risks – By signing off on a client’s ability to repay a loan, accountants expose themselves to potential legal consequences. If the client defaults, the lender may attempt to hold the accountant financially liable.

- Unfair burden – Assessing creditworthiness is the responsibility of the lender, not the accountant. Yet, many accountants felt compelled to provide these letters under pressure from their clients.

CPA Australia has long recommended that accountants decline such requests, arguing that credit assessment should rest solely with the lender.

“Some accountants are pressured by clients to sign such capacity to repay certificates,” says Belinda Zohrab-McConnell, Regulation and Standards Lead at CPA Australia.

“Regardless of how well they know the client, our recommendation has always been to refuse these requests because assessing loan repayment capacity is the lender’s job. So, we’re pleased to see this change coming into effect.”

What Should Accountants Do When Clients Request a Letter?

While ABA members will no longer require these letters, not all lenders follow the ABA Code.

- Check the lender – If the loan is from an ABA-affiliated bank, the request should no longer be made.

- If the lender is a non-bank or non-ABA member, accountants should refuse to provide the letter, as the legal risks remain the same.

- Use official guidance – CPA Australia has provided a toolkit of templates and resources to assist accountants when responding to clients requesting accountants' letters or declarations.

What About Non-ABA Lenders?

The ABA represents Australia’s 20 largest banks, including:- The four major banks (Commonwealth Bank, ANZ, NAB, and Westpac)

- Regional banks

- International banks operating in Australia

However, not all lenders follow the ABA Code of Practice.

“If a client asks for a letter, check who their lender is,” advises Zohrab-McConnell.

- If it’s an ABA-affiliated bank, they should no longer require an accountant’s declaration.

- If it’s a non-bank lender, accountants should still refuse to provide the letter, as it may expose them to legal and financial liability.

A Positive Step, But Stay Vigilant

The 2025 Banking Code of Practice is a major win for accountants, relieving them of an unfair burden and protecting them from potential legal risks. However, it is not a blanket change across the entire lending industry, non-bank lenders may still request accountants’ letters.

To protect themselves, accountants should:- Know their rights and refuse requests from non-ABA lenders.

- Educate clients on why these letters are no longer necessary.

- Use CPA Australia’s resources to navigate tricky client conversations.

As the 2025 Code takes effect, practitioners should stay informed and ensure they only engage with requests that align with professional standards and legal protections.

If you want to learn more then click the button below!

Disclaimer:

The information provided in this article is general in nature and does not constitute personal financial, legal or tax advice. While every effort has been made to ensure the accuracy of this content at the time of publication, tax laws and regulations may change, and individual circumstances vary. Dolman Bateman accepts no responsibility or liability for any loss or damage incurred as a result of acting on or relying upon any of the information contained herein. You should seek professional advice tailored to your specific situation before making any financial or tax decisions